A roof hail damage insurance claim can feel overwhelming from the moment a storm passes through your neighborhood. One day your roof appears perfectly fine. The next, you may be dealing with damaged shingles, dented gutters, water intrusion concerns, and a lengthy insurance process that seems difficult to navigate. For many homeowners, the uncertainty creates almost as much stress as the damage itself. The good news is that understanding how a roof hail damage insurance claim works can significantly improve your experience. Knowledge helps homeowners document losses properly, communicate effectively with insurance companies, and make informed decisions throughout the recovery process. While every claim is unique, the basic principles remain remarkably consistent.

Hailstorms cause billions of dollars in property damage every year across the United States. Roofing systems are particularly vulnerable because they absorb the full force of hail impacts. Even when damage appears minor, hidden issues can develop beneath the surface and create larger problems later. For homeowners in North Texas communities such as Duncanville, severe weather is a reality that cannot be ignored. Strong storms can arrive quickly, bringing hail capable of damaging even relatively new roofing systems. Knowing what to do before, during, and after the claims process can help protect both your property and your financial investment. This guide covers everything homeowners need to know about filing, managing, and strengthening a roof hail damage insurance claim.

Understanding Roof Hail Damage

Not all hailstorms are created equal. Some storms produce pea-sized hail that causes little or no damage. Others generate golf ball-sized or baseball-sized hail capable of severely damaging roofing materials within minutes.

The extent of damage depends on several factors:

- Hail size

- Wind speed

- Storm duration

- Roof age

- Roofing material

- Angle of impact

Even relatively small hailstones can create problems when combined with high winds and repeated impacts.

How Hail Damages Roofing Systems

When hail strikes a roof, it transfers energy into the roofing material. That impact can create visible and hidden damage. Visible damage often includes dents, cracks, broken shingles, and displaced granules. Hidden damage may involve weakened materials that continue deteriorating long after the storm ends. For asphalt shingles, one of the most common issues is granule loss. Those granules serve as a protective barrier against sunlight and weather exposure. Once removed, the underlying materials become increasingly vulnerable. Metal roofing systems may experience dents and deformation. Tile roofs may crack or fracture. Wood shakes can split under heavy impacts. Different materials react differently. The result, however, is often the same. Reduced roof performance and a shorter service life.

Common Types of Hail Damage

Roofing professionals typically look for several indicators when evaluating hail damage.

These include:

- Granule loss

- Shingle bruising

- Cracked shingles

- Exposed asphalt layers

- Damaged flashing

- Dented vents

- Broken skylights

- Gutter damage

- Downspout dents

Some forms of damage are immediately obvious. Others require close inspection. That distinction is important because homeowners frequently underestimate the extent of storm-related damage.

Why Hidden Damage Matters

One of the biggest challenges associated with a roof hail damage insurance claim is that serious damage does not always reveal itself immediately. A roof may look relatively normal from the ground. No leaks may be present. Everything appears fine. Months later, however, problems begin to emerge. Water infiltration. Mold growth. Interior staining. Structural deterioration. By the time these symptoms become visible, the underlying damage may already be significant. This is why professional inspections are so important after major hailstorms.

Does Homeowners Insurance Cover Hail Damage?

In many situations, yes. Most standard homeowners insurance policies provide coverage for sudden and accidental storm damage, including hail. However, coverage depends on the specific policy language. Not every roof damage claim receives the same treatment. Insurance carriers evaluate claims based on policy provisions, exclusions, limitations, and the condition of the property before the loss occurred.

What Is Commonly Covered?

Policies often provide coverage for:

- Roof repairs

- Roof replacement

- Flashing replacement

- Gutter repairs

- Siding damage

- Window damage

- Detached structures

- Interior water damage resulting from covered roof damage

Coverage varies from policy to policy. Reviewing your individual policy remains essential.

Common Coverage Exclusions

Insurance companies may deny portions of claims if they determine damage resulted from factors other than the hailstorm.

Common exclusions include:

- Wear and tear

- Lack of maintenance

- Manufacturing defects

- Improper installation

- Gradual deterioration

- Pre-existing damage

These distinctions often become central issues during claim investigations.

Replacement Cost Value vs. Actual Cash Value

Understanding your settlement type is critical. Insurance policies generally use one of two valuation methods.

Replacement Cost Value (RCV)

Replacement Cost Value coverage is designed to pay the cost of replacing damaged property with comparable materials. Depreciation may initially be withheld but can often be recovered after repairs are completed.

Actual Cash Value (ACV)

Actual Cash Value policies deduct depreciation immediately. Older roofs often receive lower settlements under ACV provisions.

Consider the difference:

| Policy Type | Roof Cost | Depreciation Applied | Initial Payment |

| RCV | $20,000 | Recoverable | Higher |

| ACV | $20,000 | Immediate | Lower |

Knowing which type of policy applies can help set realistic expectations.

What To Do Immediately After a Hailstorm

The actions taken immediately after a storm can influence the entire claims process. Panic rarely helps. Organization does.

Prioritize Safety First

Safety should always come before property concerns.

After a storm:

- Avoid climbing onto the roof

- Watch for electrical hazards

- Stay clear of unstable structures

- Be cautious around standing water

Roof inspections should be left to qualified professionals.

Document Everything

Documentation is one of the most powerful tools available to homeowners.

Take photographs of:

- Roof surfaces from safe locations

- Gutters

- Downspouts

- Siding

- Windows

- Fencing

- Vehicles

- Interior water damage

Video recordings can also be valuable. The goal is simple. Create a clear record of conditions immediately following the storm.

Preserve Evidence

If damaged materials become detached, retain them whenever possible.

Examples include:

- Broken shingles

- Damaged flashing

- Roof fragments

- Hailstones safely collected after the storm

Physical evidence can help support claim evaluations.

Schedule a Professional Inspection

Many forms of hail damage require trained eyes to identify.

Professional inspectors evaluate:

- Impact bruising

- Granule displacement

- Fractures

- Vent damage

- Flashing damage

- Structural concerns

Their findings often become critical documentation throughout the claims process.

The Roof Hail Damage Insurance Claim Process

Many homeowners expect the process to be straightforward. Sometimes it is. Sometimes it is not. Understanding the stages involved can help reduce surprises.

Step 1: Notify Your Insurance Company

Once damage is suspected, contact your insurer promptly.

Be prepared to provide:

- Policy number

- Date of loss

- Contact information

- Description of damage

- Supporting photographs

The insurer will typically assign a claim number and begin the investigation process.

Step 2: Review Your Insurance Policy

Before moving forward, carefully review your policy.

Focus on:

- Coverage limits

- Deductibles

- Exclusions

- Endorsements

- Reporting requirements

Many disputes stem from misunderstandings regarding coverage. A careful review helps establish expectations.

Step 3: Insurance Adjuster Inspection

The carrier will usually schedule an inspection.

During this visit, the adjuster evaluates:

- Roof condition

- Evidence of hail impacts

- Associated property damage

- Roof age

- Existing wear and tear

The adjuster’s findings often play a significant role in determining claim outcomes.

Step 4: Estimate Preparation

After the inspection, the insurance company prepares an estimate outlining covered repairs.

The estimate may include:

- Material costs

- Labor costs

- Equipment expenses

- Removal costs

- Disposal fees

- Applicable taxes

Homeowners should review estimates carefully. Even small omissions can significantly affect settlement amounts.

Step 5: Claim Determination

Once the review is completed, the carrier reaches a decision.

Possible outcomes include:

- Full approval

- Partial approval

- Additional investigation

- Supplemental requests

- Claim denial

A settlement offer should never be accepted blindly. Review every line item. Ask questions when necessary. Understanding exactly what is included can prevent future surprises.

Why Timing Matters

Many homeowners delay inspections because the roof appears undamaged. That delay can create complications. Evidence may disappear. Additional weather events may occur. Repair costs may increase. Questions regarding causation may arise. Prompt action helps establish a clearer connection between the storm event and the resulting damage. This becomes particularly important in regions like Duncanville where multiple severe weather events can occur during the same storm season. The sooner damage is documented, the stronger the foundation of the claim often becomes.

Common Reasons Roof Hail Damage Claims Are Denied

A denial does not always mean the damage does not exist. It often means the insurer believes the available evidence does not support coverage under the policy. Understanding why claims are denied can help homeowners avoid common pitfalls. One of the most frequent denial reasons involves wear and tear. Insurance companies may argue that roof deterioration occurred gradually rather than suddenly as a result of a hailstorm. Age frequently becomes part of that discussion. Older roofs naturally experience weathering over time. When carriers determine that deterioration existed before the storm, coverage disputes can emerge. Documentation often becomes the deciding factor.

Insufficient Documentation

Another common reason for claim challenges is inadequate documentation. Insurance companies rely heavily on evidence. Without clear photographs, inspection reports, contractor assessments, and storm-related records, proving the extent of damage becomes more difficult.

Strong documentation may include:

- Time-stamped photographs

- Inspection reports

- Repair estimates

- Weather reports

- Communication records

- Maintenance history

The more organized the information, the easier it becomes to support the claim.

Missed Reporting Deadlines

Many homeowners assume they have unlimited time to file a claim. That assumption can create problems. Insurance policies typically contain reporting requirements that require prompt notification after a loss occurs. Waiting too long can complicate investigations and raise questions about when damage actually occurred. Even if damage appears minor, scheduling an inspection sooner rather than later is generally the safer approach.

Disputes Regarding Cause of Damage

Insurance carriers do not automatically assume hail caused every roofing issue discovered after a storm.

Adjusters may evaluate alternative explanations such as:

- Wind damage

- Installation defects

- Manufacturing issues

- Foot traffic

- Age-related deterioration

When multiple potential causes exist, additional inspections and documentation often become necessary.

Cosmetic Damage Disputes

Some policies contain limitations regarding cosmetic damage. These provisions can create disagreements when dents, marks, or visible impacts affect appearance but the insurer argues functionality remains unchanged. The challenge is determining where cosmetic damage ends and functional damage begins. A seemingly minor dent may affect future performance, durability, or water resistance. Professional evaluations often help clarify these issues.

How To Strengthen Your Roof Hail Damage Insurance Claim

Successful claims rarely happen by accident. They are usually supported by preparation, organization, and persistence. Homeowners who actively participate in the process often place themselves in a stronger position.

Maintain Detailed Records

Create a dedicated claim file. Include everything.

Store:

- Inspection reports

- Photographs

- Videos

- Emails

- Letters

- Contractor estimates

- Claim notes

- Receipts

Well-organized records frequently make claim discussions more productive.

Obtain Independent Inspections

A second opinion can provide valuable perspective. Independent roofing professionals may identify damage that was not fully addressed during the initial inspection. Additional evaluations do not automatically mean the insurer made an error. However, they can help ensure all damage receives appropriate consideration.

Review Estimates Carefully

Many homeowners focus exclusively on the settlement amount. The estimate itself often contains far more valuable information.

Review every line item.

Look for:

- Missing materials

- Incorrect measurements

- Incomplete labor calculations

- Overlooked components

- Missing code-related items

Small omissions can significantly affect repair costs.

Understand Technical Findings

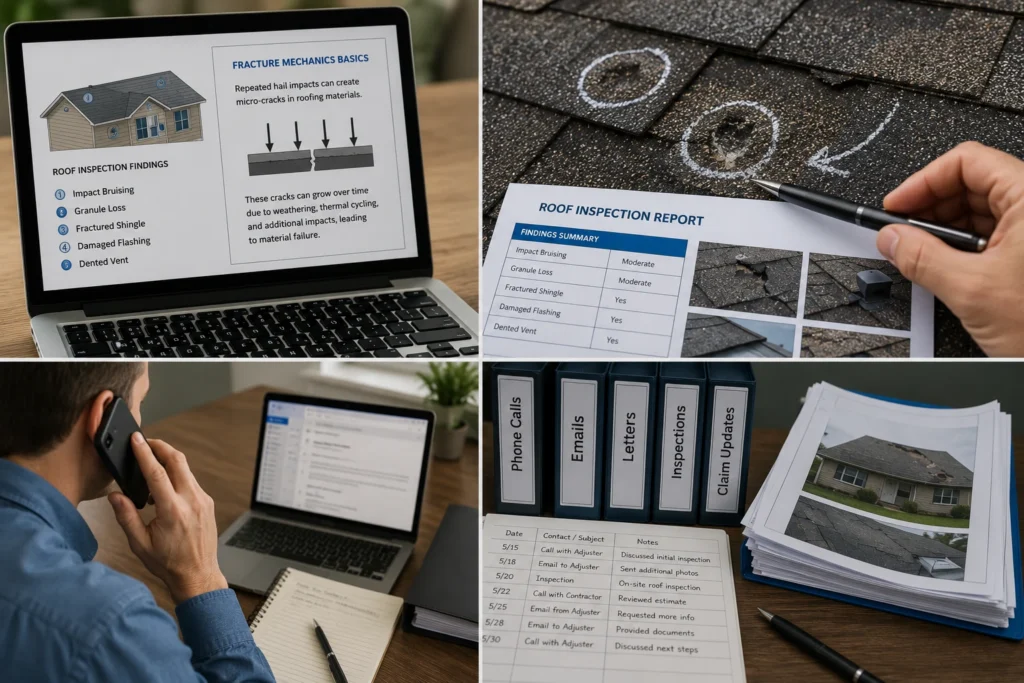

Inspection reports often contain technical terminology that homeowners rarely encounter. Learning the basics can be surprisingly helpful. For example, understanding concepts such as Fracture Mechanics can provide insight into how repeated hail impacts create weaknesses in roofing materials over time.

While homeowners do not need engineering expertise, understanding the science behind material failures can make inspection reports easier to interpret. Knowledge improves communication. Communication improves outcomes. Keep Communication Professional Insurance claims can become stressful. Emotions are understandable. However, maintaining professional communication often produces better results.

Keep records of:

- Phone calls

- Emails

- Letters

- Inspection appointments

- Claim updates

A documented communication history can become valuable if questions arise later.

Roof Repair vs. Roof Replacement

One of the most important decisions during a roof hail damage insurance claim involves determining whether repairs are sufficient or whether full replacement is necessary. The answer depends on the extent of damage.

When Repairs May Be Appropriate

Repairs are often considered when damage remains limited to specific areas.

Examples include:

- Isolated shingle impacts

- Minor flashing damage

- Small affected sections

- Localized roof slopes

In these situations, repairing damaged areas may adequately restore performance.

When Replacement May Be Necessary

More extensive damage often supports replacement.

Factors may include:

- Multiple damaged roof slopes

- Significant granule loss

- Widespread bruising

- Matching issues

- Structural concerns

A roof functions as a complete system. Sometimes repairing individual sections does not provide a practical long-term solution.

Factors Insurance Companies Evaluate

Insurance carriers often consider several factors when determining repair scope.

| Factor | Influence on Decision |

| Roof Age | Older roofs may require additional evaluation |

| Material Type | Different materials respond differently to hail |

| Extent of Damage | Widespread impacts increase replacement potential |

| Repairability | Availability of matching materials matters |

| Local Codes | Building regulations may affect scope |

Every claim is unique. No single formula applies to every property.

Challenges Homeowners Commonly Face

Even valid claims can encounter obstacles. Understanding common challenges allows homeowners to prepare more effectively.

Underpaid Claims

Not all disputes involve outright denials. Sometimes coverage is approved, but settlement amounts appear insufficient.

Potential causes include:

- Missing line items

- Incomplete damage scopes

- Incorrect measurements

- Underestimated labor costs

- Missing accessories

Reviewing estimates carefully can help identify these issues.

Delayed Claim Decisions

Insurance investigations occasionally take longer than expected.

Delays may result from:

- High claim volume

- Additional inspections

- Engineering reviews

- Documentation requests

- Weather-related workloads

Patience is often necessary. However, regular follow-up can help maintain momentum.

Conflicting Assessments

Different professionals sometimes reach different conclusions. A contractor may identify extensive damage. An adjuster may identify less. This does not automatically mean either party is wrong. Different observations, methodologies, and interpretations can produce different findings. Resolving disagreements often requires additional evidence.

Communication Difficulties

Many homeowners simply want clear answers. Unfortunately, insurance terminology and claim procedures can sometimes feel complicated. Asking specific questions and requesting written explanations can improve clarity. The goal is understanding. Not assumptions.

The Role of a Public Adjuster

Many policyholders do not learn about public adjusters until after a major property loss occurs. Yet they can play an important role in certain claims.

What Does a Public Adjuster Do?

A public adjuster is a licensed insurance claims professional who represents policyholders.

Their responsibilities may include:

- Reviewing insurance policies

- Evaluating damages

- Organizing documentation

- Preparing claim presentations

- Assisting with negotiations

Unlike insurance company adjusters, public adjusters work on behalf of the property owner.

Public Adjusters vs. Insurance Adjusters

The distinction matters.

| Public Adjuster | Insurance Adjuster |

| Represents policyholder | Represents insurance company |

| Evaluates claim from insured’s perspective | Evaluates claim for carrier |

| Assists with documentation | Reviews submitted information |

| May negotiate claim issues | Makes claim recommendations |

Understanding these roles helps homeowners make informed decisions.

When Professional Assistance May Help

Certain situations can become particularly complex.

Examples include:

- Large losses

- Denied claims

- Underpaid claims

- Multiple damaged structures

- Significant scope disputes

Professional guidance may help homeowners better understand their options. Some policyholders who have previously worked with a Fire Insurance Adjuster following a fire-related loss are often surprised to learn that similar claim advocacy services exist for hail and storm damage claims as well.

Understanding Hail Damage Inspection Reports

Inspection reports are often among the most important documents in the entire claims process.

Unfortunately, many homeowners glance at them briefly and move on.

That can be a mistake.

A thorough inspection report often contains:

- Damage photographs

- Roof diagrams

- Material assessments

- Measurements

- Impact locations

- Repair recommendations

These reports help establish the scope of damage and provide supporting evidence for claim evaluations. Carefully reviewing inspection findings can reveal important details that may affect settlement discussions later. Supplemental Claims and Additional Damage Discoveries Not every problem is visible during the initial inspection. As roofing contractors begin repairs, additional damage sometimes becomes apparent.

Examples may include:

- Damaged decking

- Hidden moisture intrusion

- Ventilation issues

- Additional flashing damage

- Structural concerns

When covered damage is discovered after the original claim review, homeowners may be able to submit a supplemental claim. A supplemental claim is not a new claim. It is a request for additional compensation based on newly identified covered damage. Proper documentation remains essential.

Common Mistakes Homeowners Make After a Hailstorm

Avoiding mistakes can strengthen a roof hail damage insurance claim significantly.

Common errors include:

- Delaying inspections

- Taking limited photographs

- Failing to preserve evidence

- Ignoring minor damage

- Overlooking related property damage

- Failing to review estimates carefully

Seemingly small decisions often have larger consequences later. Proactive action usually produces better results.

How Insurance Companies Calculate Roof Depreciation

Depreciation plays a major role in many claims. Insurance companies may evaluate:

| Factor | Potential Impact |

| Roof Age | Older roofs often receive greater depreciation |

| Material Type | Lifespan varies by material |

| Current Condition | Existing wear affects valuation |

| Maintenance History | Maintenance can influence evaluations |

| Expected Lifespan | Longer-lasting roofs depreciate differently |

For Actual Cash Value policies, depreciation directly affects claim payments. For Replacement Cost Value policies, recoverable depreciation may become available after repairs are completed and properly documented. Understanding depreciation helps homeowners interpret settlement offers more effectively.

Roof Hail Damage Claims in Duncanville

Severe weather is a familiar concern throughout North Texas. Communities such as Duncanville regularly experience storms capable of producing damaging hail. These weather events can affect roofing systems regardless of age or material type.

Why Prompt Action Matters

After major storms, roofing contractors, inspectors, and insurance professionals often experience increased demand. Waiting too long can create complications. Evidence may deteriorate. Additional storms may occur. Repair costs may increase. Prompt inspections help preserve valuable information and strengthen claim documentation. For many homeowners in Duncanville, early action becomes one of the most important factors in a successful claim experience.

Preventing Future Hail Damage

No roofing system is completely immune to hail. However, homeowners can reduce risk through proactive maintenance and strategic upgrades.

Schedule Regular Inspections

Annual roof inspections can identify developing issues before they become major problems.

Routine inspections may reveal:

- Loose shingles

- Flashing problems

- Vent damage

- Early deterioration

Addressing small issues early often prevents larger expenses later.

Consider Impact-Resistant Roofing Materials

Many homeowners evaluate impact-resistant products after experiencing storm damage.

Potential benefits include:

- Improved durability

- Better hail resistance

- Longer service life

- Potential insurance incentives

While no material guarantees protection, some products perform significantly better during severe weather.

Maintain the Entire Roofing System

Roof performance depends on more than shingles.

Regular maintenance should include:

- Gutter cleaning

- Flashing inspections

- Vent inspections

- Tree trimming

- Drainage evaluations

A well-maintained roof generally performs better when severe weather arrives.

Final Thoughts

A roof hail damage insurance claim involves far more than reporting damage and waiting for a settlement check. The most successful claims are built on preparation, documentation, organization, and persistence. Homeowners who understand their policies, document damage thoroughly, communicate effectively, and act promptly often place themselves in a stronger position throughout the claims process. Hail damage is frequently more serious than it first appears. What looks like a few dents or missing granules may eventually develop into leaks, structural concerns, and expensive repairs if left unaddressed. That is why inspections matter. Documentation matters.

Understanding the process matters. For homeowners throughout North Texas and communities like Duncanville, severe weather remains an ongoing reality. While no one can prevent hailstorms, property owners can prepare for what happens afterward. When damage is suspected, act quickly. Document thoroughly. Review your policy carefully. Seek professional guidance when necessary. Most importantly, remember that protecting your roof means protecting your home, your investment, and your peace of mind. A properly managed roof hail damage insurance claim can help ensure that recovery happens as smoothly and efficiently as possible.

FAQs

Common signs include dented gutters, granule loss, cracked shingles, and water stains inside the home. A professional inspection can confirm the extent of damage.

The deadline depends on your insurance policy and state regulations, but it’s best to report damage as soon as possible after a storm.

Most homeowners insurance policies cover sudden hail damage, but coverage depends on your policy terms, exclusions, and roof condition.

Yes. A professional inspection can identify damage, provide documentation, and help determine whether filing a claim is appropriate.

You can submit additional documentation, request a reinspection, or seek an independent evaluation to support your claim.

Yes. Hidden damage may weaken roofing materials and allow moisture intrusion long after the hailstorm has passed.

Repairs address localized damage, while replacement is often necessary when hail damage is widespread or affects multiple roof sections.

Yes. Supplemental claims may be submitted when additional covered damage is found during repairs or further inspections.

Not necessarily. Premium changes depend on several factors, including your insurer, claim history, and regional storm activity.

A public adjuster may help with complex, denied, or underpaid claims by assisting with documentation and claim evaluation.